The Bank of England looks set to hike rates for a third time in March, and there’s nothing much in the latest jobs report that’s likely to change that.

Redundancies are remarkably low, and the unemployment rate, at 4.1%, is as close to pre-virus levels as to make no difference. Unfilled vacancies are unusually high. And wage growth, though recently steadier, is back to pre-virus rates, which in themselves were consistent with a tight jobs market. Omicron doesn’t appear to have changed the overall story, though we’ll have to wait for another couple of reports for the definitive answer.

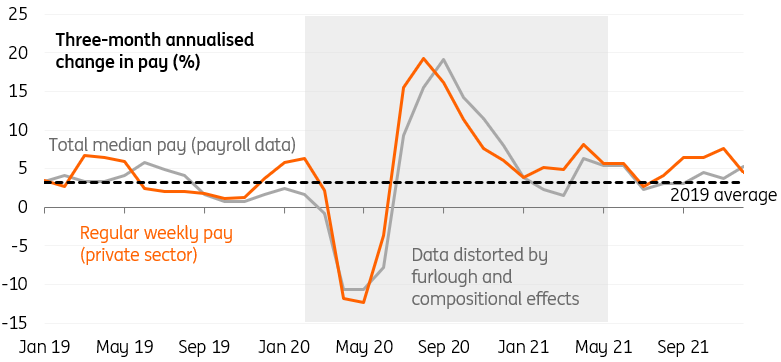

Wage growth has stabilised over recent months

However, we still doubt that the UK is headed for a wage-price spiral that would justify the six rate hikes markets are now expecting from the BoE this year.

Much of the recent debate has focused on workers making higher wage demands in response to the rising rates of headline inflation. But remember that only around 30% of UK employees are covered by collective bargaining, compared to 70%+ in many other Western European economies, according to EU data.

That means there’s a less direct route from higher CPI to wages, and instead, the process relies more on workers quitting their jobs to protect their disposable incomes, or employers raising pay to stop them from doing so. In the UK’s case at least, higher inflation expectations probably matter less for wages than whether the jobs market continues to tighten.

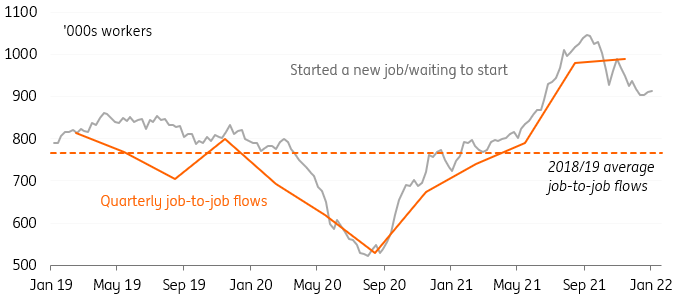

There is some evidence that this process is happening. Job-to-job flows were very high through the autumn, though more recently the number of people waiting to start a new job has begun to fall.

Job-to-job flows increased as the economy reopened but have begun to slow

One explanation is that a lot of the churn last autumn simply reflected the jobs market coming out of a very dormant phase. Even accounting for the recent spike in job-to-job flows, we estimate that 120k fewer people have moved jobs since the start of 2020, compared to what might have happened had pre-virus trends continued. People unsurprisingly moved roles less while uncertainty was high and hiring demand low.

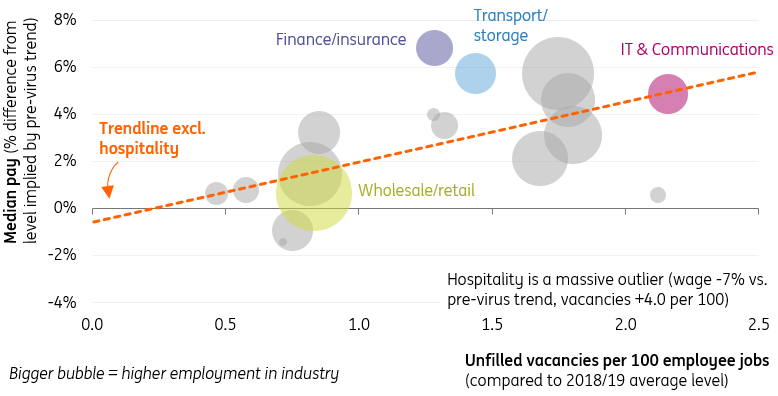

In other words, the jobs market has been playing catch-up, and we think some of the recent wage pressures have been borne out of this state of (probably temporary) flux. Our chart below shows that pressures are more prevalent in sectors where unfilled vacancy rates are further above their pre-virus averages.

Above-trend pay growth is more common in industries where vacancy rates are higher than pre-virus

That’s often in places where consumer spending trends have changed abruptly over the past couple of years – be it the switch to online retail, or the abrupt resurgence in demand for hospitality last summer. Data from hiring agency Indeed shows huge annual pay rises for lorry drivers and chefs, but overall wage growth is more stable.

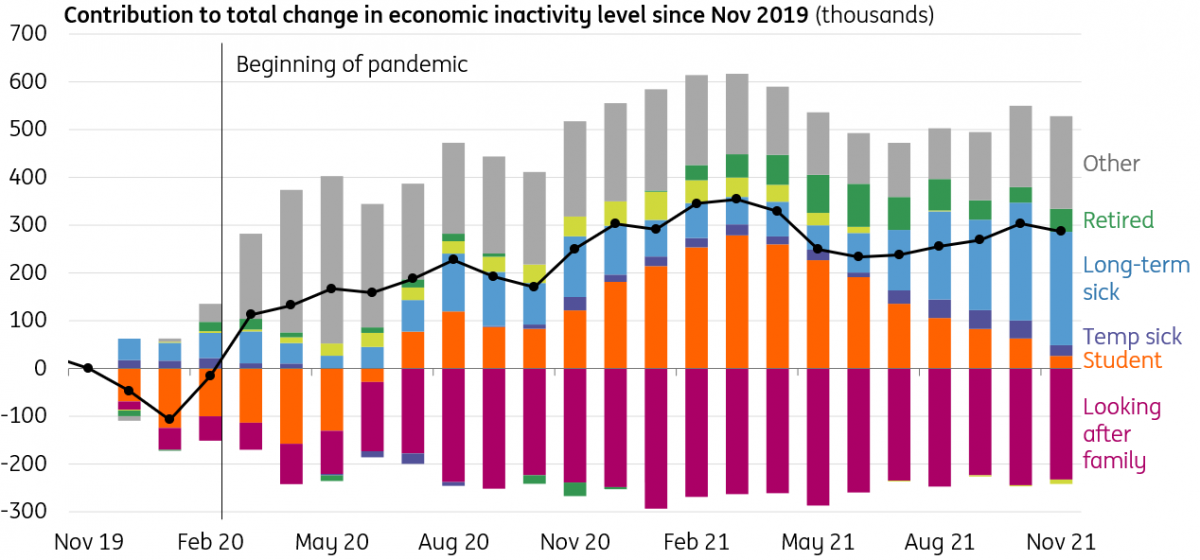

Economic inactivity is another potential source of recent worker shortages. Like we’ve seen in the US, there’s been a pronounced increase in the number of working-age people neither in nor actively looking for work since the pandemic began. But unlike the US, where a lot of this trend has been attributed to early retirements, it’s long-term sickness rates that have risen and helped prevent UK employment from reaching pre-virus levels. How much of this is linked to long-Covid is not yet clear.

The overriding message is that we should be cautious in extrapolating trends in the jobs market from late last year for the UK wage growth outlook. None of this is to say that wage growth can’t rise further, especially in the short term. Indeed we think the current backdrop will lead the Bank of England to hike rates again at the next two (maybe even three) consecutive meetings.

But as the mismatch in the jobs market dissipates following last summer’s reopenings, so too should some of the related pay pressures. The inactivity story is trickier to forecast, but there is a scenario where more people return to the jobs market, which should also help to ease some of the recent pressures.

Incidentally, all of this is largely what the Bank of England’s February forecasts showed too. That policymakers were forecasting a gradual slowdown in wage growth and an increase in unemployment over coming years should be read as a subtle hint that market rate hike expectations have gone too far.

Long-term sickness has offset falling student numbers to keep inactivity levels high

Source: ING

PG-Software

PG-Software